- Combination of rapid growth and margin hikes are key

- Regulatory backcloth seen as very supportive

- Profits breakthrough predicted in the past, and missed miserably

Listed on the London stock market for nearly 20 years, yet it has never made a profit, Seeing Machines (SEE:AIM) is one of those small cap stocks that investors tend to love or hate.

We know that the global automotive industry has been at the forefront of automation technology for decades and this remains the case, but with full self-driving technology still being tested, and to a large degree, untrusted, Seeing Machines’ driver monitoring system, or DMS, has the capacity for significant growth over the coming years… at least, that’s Berenberg’s view.

Among other things, DMS can alert drivers when they are in danger of nodding off at the wheel, a major killer, and so prevent hundreds if not thousands of deaths annually.

‘We see potential for the firm to offer a multi-year revenue growth story, driven by the increased penetration of DMS in various elements of the global transportation network,’ said Berenberg in its latest note to clients. ‘We also think higher-margin royalty revenues will become a larger part of the mix, supporting gross margin expansion.’

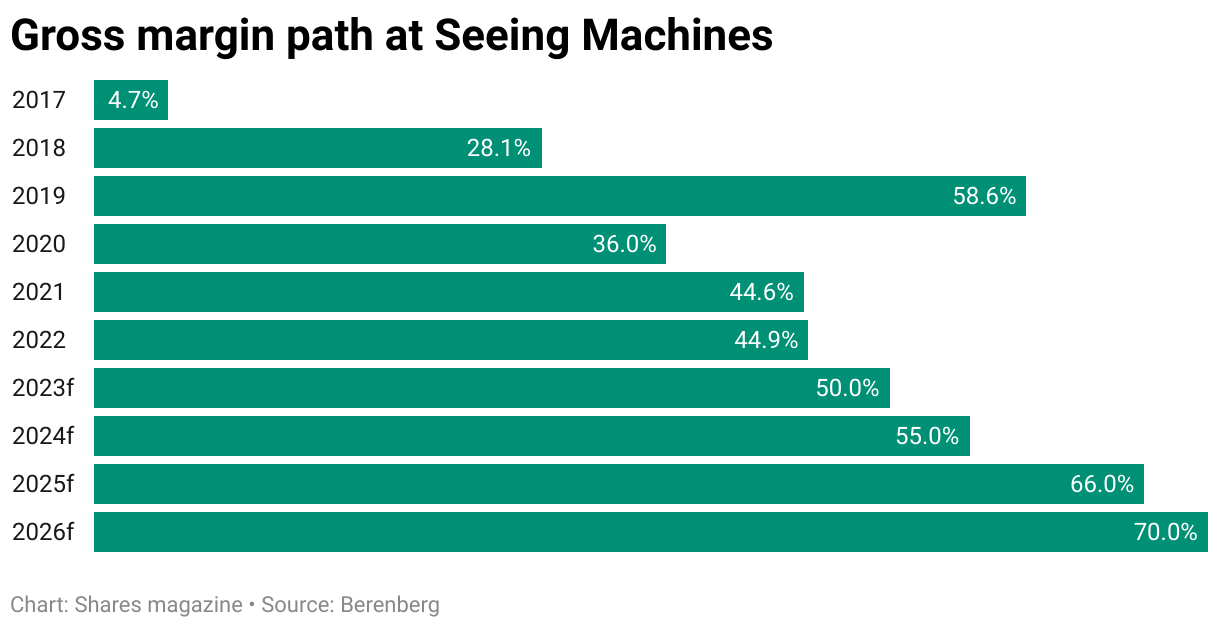

Gross margins last year were 44.9% but are set to hit 50% in 2023 (to Jun) and surge to 70% over the following three years, according to Berenberg projections.

WHAT IS BERENBERG’S THESIS?

‘Despite it being relatively early in Seeing Machines’ prospective growth evolution, we note that regulatory tailwinds and a largely contracted revenue profile underpin significant parts of the growth story,’ the analysts say.

For example, the investment bank believes in the coming decade that the proportion of global auto production shipped, including some component of DMS, will increase from under 10% to north of 70%, creating significant opportunities for a business that has historically had a 30% to 40% market share.

‘We also believe the high-margin royalty revenue received for every DMS-fitted car that is manufactured will continue to grow and create a more resilient future earnings stream. This has already helped drive an improvement in gross margins from 28% in full year 2018 to 45% in 2022, but we think they can reach 70% by 2026.’

WILL PROFITS FINALLY ARRIVE?

This implies breakeven for the business in 2025 as the combination of high top-line growth and increasingly high gross margin revenue mix leads to strong growth in gross profit, or so Berenberg believes.

‘We believe the economics of the business model could support an EBITDA (earnings before interest, tax, depreciation and amortisation) margin in the 25% to 30% range at scale.’

However, investors have been here before. Back in 2015, analysts at FinnCap were predicting a profits breakthrough by 2018, and that failed miserably. Where FinnCap had forecast an adjusted pre-tax profit of A$17.6 million, the company end up reporting a A$36 million pre-tax loss.