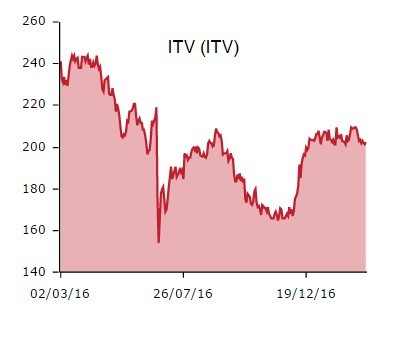

Free-to-air broadcaster ITV (ITV), one of Shares' big picks for 2017, gains 2.1% to 207p as full year results come in ahead of forecasts. This positive news is somewhat undermined by a weak outlook for advertising revenue.

As we warned when previewing the results, the company faces tough comparatives in the first part of 2017, partly thanks to the timing of Easter. Guidance is for advertising revenues to fall 6% in the first four months of the year.

EARNINGS BEAT

More positively 2016 earnings per share came in at 17p against consensus at 16.3p, the dividend is hiked 20% year-on-year to 7.2p and there is a special dividend of 5p on top. And advertising revenue comparatives get easier for ITV as the year progresses.

Liberum analyst Ian Whittaker who counts ITV as his top ‘buy’ in the media sector with a 340p price target says: ‘The TV advertising environment is the obvious unknown but, as we have pointed out, the current economic outlook does not suggest that there should be a major advertising decline, which consensus 2017 forecasts seem to be suggesting.

‘The advertising performance year to date should be enough to satisfy concerns given April's performance and the comments on Studios should reassure as should ITV1's audience share performance (+3%). Moreover, the continued growth of high margin online revenues will help drive earnings growth.’

‘M&A BACKSTOP’

Investec analyst Steve Liechti says: ‘Full year figures are above our forecasts and there is a new 5p special dividend, but four month national advertising revenue outlook at -6% is worse than we hoped.

'Shares have partly discounted this, and we see an M&A backstop with weak sterling making high profile UK media assets attractive.’