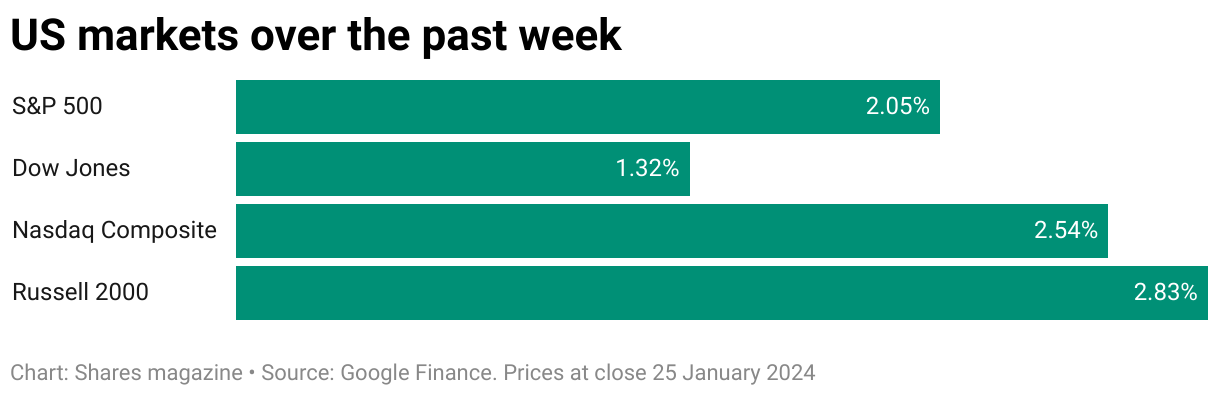

Helped by positive news on the economy, US markets had another strong week with the S&P500 index, the Nasdaq Composite and the Dow Industrials making new all-time highs.

Real GDP (gross domestic product) expanded at an annual rate of 3.3% in the fourth quarter, marking a slowdown from the previous quarter’s 4.9% but above consensus forecasts of 2% suggesting the US economy remains on track for a ‘soft landing’ where the Federal Reserve contains prices without constricting growth.

Once again, the consumer was the main driver of growth contributing 1.9% to the GDP figure as the buoyant labour market continues to support household spending.

Also pleasing was fourth-quarter core PCE (personal consumption expenditure), which is the Fed’s preferred measure of inflation rather than the CPI (consumer price index) and which came in at 2%, in line with forecasts and the official target rate, indicating that higher interest rates are having the desired effect of bringing inflation under control.

Interest rates are widely expected to remain at their 20-year high of 5.25% to 5.5% at next week’s central bank meeting, but this latest data should give policymakers more room to decide on the eventual pace of potential cuts.

INTEL

Computer chip giant Intel (INTC:NASDAQ) posted better-than-expected fourth-quarter sales and earnings last night, but its outlook for the first quarter of 2024 was a big disappointment sending its shares down $5.40 or 11% to $44.15 in after-market trading.

Sales for the final three months of 2023 were up 10% at $15.4 billion against forecasts of $15.2 billion, led by client computing which posted revenue of $8.8 billion, $400 million above expectations.

Earnings per share were also comfortably ahead of the consensus at 63c instead of 45c thanks to increased operational efficiency after the firm took out $3 billion of costs last year.

However, its first-quarter guidance came up significantly short of market expectations, with earnings per share seen at 13c against the consensus of 34c and sales seen between $12.2 billion and $13.2 billion, well short of the Zacks forecast of $14.25 billion.

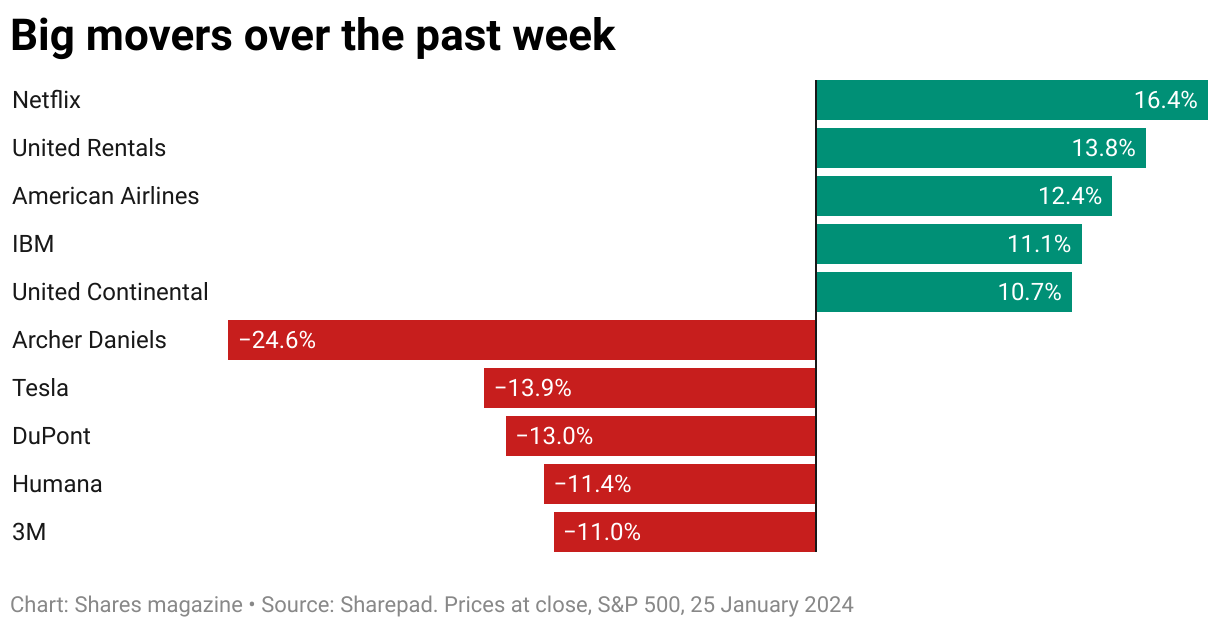

NETFLIX

It may seem a little premature to call victory for Netflix (NFLX:NASDAQ) in the vicious TV streaming wars, but Q4 2023 numbers over the past week felt like a big step towards that end. More than 13 million net new subscribers, $6.9 billion of free cash flow, guidance for higher operating margins – this is far more meaningful to investors than the 18 Oscar nominations bagged this week.

The stock surged 11% in response this week, then rallied again to hit $562, heights not seen in more than two years and harking back to when we were all locked down. Netflix has emerged as one of consumers’ essential services, meaning it has pricing power, and that’s a tune investors are happy to chime in with.

So, what next? Plenty it seems. Gaming is growing nicely, while it has moved beyond dipping its toe into sports waters signing a $5 billion 10-year deal to exclusively broadcast World Wrestling Entertainment’s Raw from January 2025 across the US, Canada, UK, and Latin America, giving even more reason for subscribers to stick with the platform.

TESLA

Amid this weeks’ relative market optimism, Elon Musk’s EV (electric vehicle) giant stuck out like a sore thumb. No one doubts Tesla (TSLA:NASDAQ) is in for an uncomfortable journey as it makes the switch from being a high-end, high-margin, specialist automaker to a mainstream giant.

Never mind the modest miss on Q4 2023 earnings and revenues, the gloom came after the company accepted that its previous 2.2 million unit deliveries target this year was too ambitious and that consumers’ pockets can be mined only so far.

There was talk of a new sub-$25,000 model, codenamed Redwood at this stage, and likely set for a late 2025 or 2026 launch, while Cybertruck sales will be keenly watched through the coming months. For now, it appears, investors are happy to bank some of the steep profits earned by the share price doubling last year.