We have confirmation today that previous revenue growth ambitions of NetDimensions (NETD:AIM) have shifted further out, not hugely surprising since the company continues to grapple with the crimp on growth from its own cloud transition.

There's been a $50 million revenue target in place for a few years now (read details here), but while analysts' early projections were for perhaps 2017 (the full year to 31 December) or 2018, management reckon 2019 is now more likely.

'We are conservative, we're not trying to blow hot air and set ourselves up for a fall,' says CFO Matthew Chaloner.

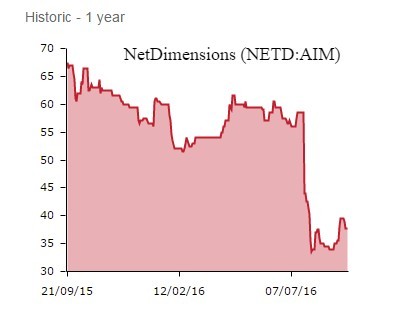

The challenges facing the talent management and training software supplier came to a head in July, the company issuing a profit and revenue warning that slapped 28% off the share price on the day (which you can read about here).

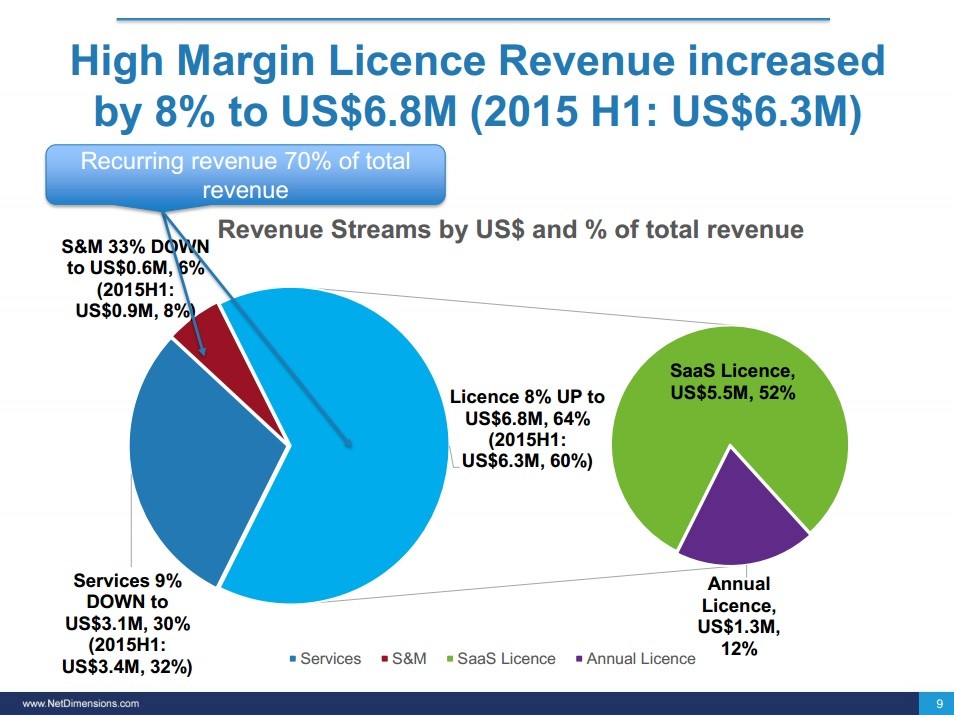

Today's half-year figures put more meat on the bones. You can read the details for yourselves, although the below graphic from the company's presentation provides a neat snapshot.

Existing customers 'all have their own challenges,' explained CEO Jay Shaw to Shares today, some macro and competition related, others regulatory, understandable in the rules-laden high consequence niche where NetDimensions concentrates.

One of the bigger threats to the $50 million revenue target is acquisitions. A small handful were always part of the strategy and growth objective, finding ones that fit just so isn't easy. We have 'struggled to find the right kind of acquisitions,' says CFO Matthew Chaloner. That may irk some investors but better to buy nothing at all than throw money at the wrong business for the sake of it.

'We shave full year revenue by $0.5 million and EBITDA estimates by around $0.2 million, reflecting ongoing timing effects,' says Panmure Gordon analyst Jonathan Helliwell. 'This now implies a marginal EBITDA loss in the current year, moving into profitability in full year 2017.'

With $11.2 million net cash on the books, the analyst calculates a NetDimensions enterprise value/sales of 0.5-times, 'a substantial discount to larger peers,' Helliwell reckons. That after the shares stayed virtually unchanged today at 37.25p. 'This points to strong long term upside potential as the group moves towards its $50 million revenue target and into profitability.'