- Final dividend of 3.15p

- Share price return falls by 7%

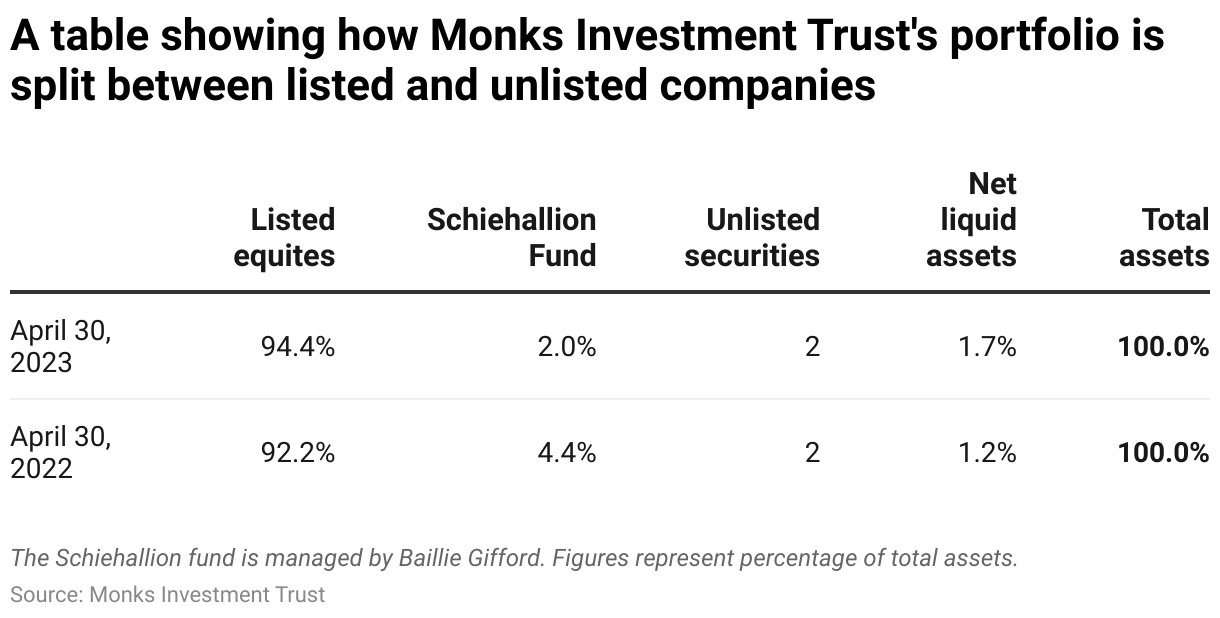

- Unquoted companies exposure reduced to 4%

Monks Investment Trust’s (MNKS) net asset value for the year ending 30 April 2023 fell by 1.6% and underperformed its benchmark, the FTSE World Index.

The share price total return fell by 7% compared to a 3.2% increase in the FTSE World Index.

The Edinburgh-based investment trust blamed its performance on growth stocks which dragged down any cumulative gains made from previous years.

The trust, which is managed by Baillie Gifford, also admitted that ‘mistakes have been made’ in the past.

Monks’ investment managers Spencer Adair and Malcolm MacColl said they are now committed to ‘drive positive returns for investors over the long-term.’

A single final dividend of 3.15p has been declared, an increase from 2.35p last year.

PAST PERFORMANCE

This contrasts with Monks’ performance over an eight-year period, when the trust changed its investment approach with the appointment of new managers Spencer Adair and Malcolm MacColl.

Adair and MacColl have adopted a ‘bottom up’ global stock picking approach.

Since the end of March 2015, the NAV total return is up 126.7% against the comparative index at 127.4% while over the same period the share price total return was up 131.3%.

REDUCING EXPOSURE TO UNQUOTED COMPANIES

Monks has come under fire like other Baillie Gifford-run trusts such as Scottish Mortgage Investment Trust (SMT) due to its exposure to early stage, rapid growth and unquoted companies, which are deemed higher risk.

Unquoted companies are deemed riskier because they are not traded on the open market and are highly illiquid for those investing in them. Iain Scouller, an analyst at Stifel, noted that Monks in the past had 40% exposure to rapid growth companies which it has since reduced to 30% to reflect the difficult environment.

Chairman of Monks, Karl Sternberg, said: ‘We currently take comfort from the low exposure of Monks to unquoted companies, which represent 3.9% of total assets: 2% by way of the Schiehallion fund, a publicly traded investment company; and 1.9% through direct investment.’

Sternberg maintains the benefits of having unquoted companies in Monk’s holdings saying they are ‘the fastest-growth companies’ and it allows ‘exposure to some of the best companies driving economic change.’

However, Sternberg says there are drawbacks because unquoted companies ‘have high financing needs' and that represents a risk in today's environment of tightening liquidity and competition for funds.’

Schiehallion's shares currently trade at a discount to net asset value, which Sternberg says, ‘offers the potential for re-rating should sentiment towards growth capital improve.’

STIFEL ANALYST UPBEAT

Iain Scouller, analyst at Stifel said Monks’ ‘flattish return’ is ‘reasonable considering ‘the difficult environment for many growth stocks over the past year.’

‘We think this remains a good vehicle to use to access growth companies, but with lower exposure to unquoted [companies] at circa 4% of the portfolio. The shares are trading on around a 12% discount and we retain a neutral recommendation.’

LEARN MORE ABOUT MONKS