It's a busy old day in the UK mobile telecoms space. There's a new satellite IPO, as Satellite Solutions (SAT:AIM) reverses into cash shell Cleeve Capital and raises £2.25 million at 4.5p per share. The stock is now trading at 5p, or 11% up.

Then there's nine-month figures from satellites operator Avanti Communications (AVM:AIM), which leaves the company needing a pretty gang-busters fourth quarter to meet EBITDA (earnings before interest, tax, depreciation and amortisation) estimates of $10.8 million, according to consensus, given the third quarter's $1.6 million positive figure being offset by a first half $3.5 million EBITDA deficit.

Investors have tended to either love this share, or loathe it, and clearly the bulls are in the box seat today, with the stock 5.5% higher at 243.25p.

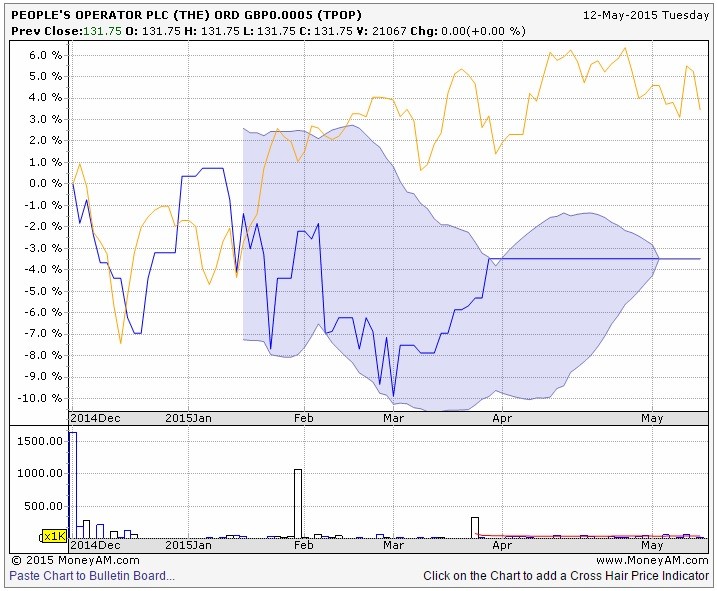

But perhaps most interesting are full year 2014 figures for The People's Operator (TPOP:AIM), which joined AIM on 4 December, raising £20 million at 130p per share in the process. Regular Shares readers may recall the company, we looked at it in some depth in a feature on 2 April, which you can read here.

We were rather sceptical then, and it's hard to look any more positively on the story now.

This is the mobile virtual network operator (MVNO) that gives a portion of benevolent-feeling customer bills to charity, and a slug of its own profits too. The results show rapid growth, albeit from a low base, in subscribers, doubling since the December year-end to 30,000, having posted a 140% jump in the second half of last year. A US launch is coming soon. Go go the do-gooders!

But what does this translate into, you might wonder. Certainly not very much. Revenues were £432,391 last year, roughly 55% of the cost of those very sales. Add in distribution charges, admin expenses, salaries etc, operating losses total £2.3 million. Fair's fair, it's very early days operationally so making hard and fast judgements on performance is a bit harsh.

But what investors do need to do is consider the premium for implied upside. On a flat share price of 131.75p today, the company has a market value of £101.6 million.

Strip out the £18.4 million net cash, you're looking at an enterprise value (EV) to EBITDA of 4.4-times for 2016. That's assuming the estimates $5.5 million negative EBITDA this year can be turned into a $19.1 million positive next year.

Look at it another way, as those helpful analysts at IT and communications research boutique Megabuyte point out. Tesco (TSCO) is reported to be selling its own MVNO, and applying The People's Operator metrics would imply a very doubtful £13 billion, based on its 4 million subscribers. No, I can't see them getting anything like that either.