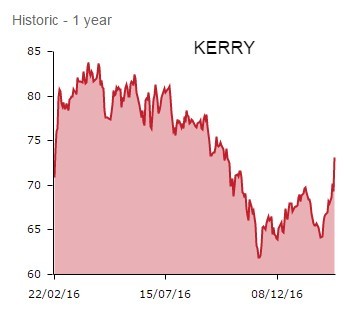

Ireland-based ingredients-to-packaged foods play Kerry (KYGA) is nourishing investors’ portfolios today. News of a forecast-busting fourth quarter combined with a solid outlook statement sends the shares 4.7% higher to €72.58.

A global manufacturer of ingredients and flavours for the food and beverage industry and supplier of branded and private-label packaged foods, Kerry is in demand after serving up organic volume growth of 4.9% for the final quarter of calendar 2016, smashing Bloomberg consensus expectations for 2.1% growth.

TASTY MOMENTUM

Full year results reveal a modest top line increase to €6.1bn for the year, good volume growth helping Kerry offset adverse currency moves and lower pricing. However investors are excited by the fourth quarter performance, demonstrating that Kerry is carrying momentum into 2017.

In Q4, the Taste & Nutrition arm delivered impressive 5.6% volume growth, its performance boosted by excellent growth in developing markets including China, Indonesia, Vietnam and the Philippines. Recent acquisition Jungjin Foods is also enlivening growth in South Korea. Meanwhile, the Consumer Foods division generated resolute 1.7% volume growth in Q4. Kerry is outperforming peers thanks to a repositioning of the product offering to tap into the snacking, convenience and food-to-go trends.

As Shares outlined here, the Dairygold spreads-to-Richmond sausages maker operates in some sluggish end-markets, yet it is outflanking rivals through a focus on growth categories and innovation.

Significantly, the industry is crying out for the value-added services Kerry offers - it is locked into customers' supply chains and helps them reduce both costs and time-to-market for new products.

CONFIDENT CASH COW

Kerry delivered margin expansion and record free cash flow (FCF) of €570m in 2016, up from €453m in 2015, enabling it to invest in product innovations and propose a plump 12% hike in the total dividend to 56 cents.

Also announcing that Edmond Scanlon, who heads up the Asia Pacific business, will take over as CEO on Stan McCarthy’s retirement in September, Kerry issues a reassuringly solid outlook statement for 2017. Management expects Kerry to ‘achieve good revenue growth and 5% to 9% growth in adjusted earnings per share to a range of 339.6 to 352.5 cent per share (2016: 323.4 cent per share).’

Moreover, the broker explains: ‘As Kerry’s customers go through a major churn in their product portfolio, the strong ingredients platform allows the group to take market share, improve mix and enhance margins. Accretive bolt-on M&A is a key driver - we estimate Kerry has €1.5bn+ firepower available to consolidate the ingredients market.'