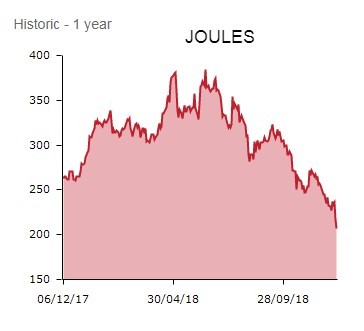

Premium British lifestyle brand Joules (JOUL:AIM) is in investors good books on Wednesday, the share price sparking up 9.2% to 226p on the news first half profits will beat market expectations.

A differentiated brand in an upgrades cycle, Joules’ rapid growth is in stark contrast to much of the wider retail sector. However, the company’s level-headed management team is staying grounded, cautioning ‘trading conditions in the UK will remain challenging over the near term, with continued macroeconomic uncertainty, rapidly changing consumer shopping behaviours and a highly competitive environment.’

JOULES CROWNED BY INVESTORS

In a well-received trading update, the clothing, accessories and homeware brand established by Tom Joule nearly three decades ago, says it expects underlying pre-tax profit will come in ‘slightly ahead of initial expectations’ for the half to 25 November.

Despite a very tough prior year comparator, sales grew by a healthy 17.6% to £113.1m in the half, reflecting the strength of the Joules brand, enviable overseas growth and the broad appeal of its products.

Market Harborough-headquartered Joules operates 123 stores in the UK and Republic of Ireland, boasts a significant online business and has a wholesale business with over 2,000 stockists worldwide, John Lewis and Nordstrom among them.

The international business now speaks for 16% of the top line total, up from 11.3% a year ago and driven by hearty appetite for the brand in Germany and the US. The latter territory is ‘delivering further super-normal growth as the product proposition resonates across existing and new accounts’, enthuses Liberum Capital.

TOTAL RETAIL MODEL

Joules also attributes its strong revenue showing to a flexible ‘total retail’ model that is tapping into changing shopping patterns.

This means the delivery of a seamless and enjoyable experience to customers, ‘irrespective of how, when and where they want to shop the Joules brand’, according to the company. ‘E-commerce performed particularly well in the first half and now represents nearly 50% of all retail sales.’

CEO Colin Porter says the forecast-beating showing ‘is testament to the strength of the Joules brand, the engagement of our loyal customers with our product collections, and our fantastic teams’ and is looking forward to the second half with confidence, believing his charge can achieve full year profits in line with the board’s expectations.

Joules has also put contingency plans in place to mitigate any disruption that could arise in the event of a ‘hard Brexit’, establishing an EU based third party distribution facility, scheduling earlier inbound product deliveries for Spring/Summer 2019 ranges and hedging its US Dollar requirements more than 12 months forward.

Liberum Capital comments: ‘While today’s update is encouraging with first half underlying pre-tax profit now expected to be slightly ahead of management’s expectations, we leave our full year forecasts unchanged ahead of the key Christmas trading period.

‘Joules needs to achieve second half revenue growth of 13.8% (versus the 17.6% achieved in the first half) to meet our full year sales forecast. This leaves the group well positioned to achieve our full year 2019 underlying PBT forecasts of £14.8m, which represents year-on-year growth of 14.7%.’

The brokerage adds: ‘Joules has a strong brand, heritage, low fashion risk and wide appeal. It is gaining share in the fast-growing premium lifestyle sector where multiple growth levers exist including stores, online, wholesale and international. Joules is relatively immature versus key peers leaving space for growth.'