Cut-price general merchandise seller B&M European Value Retail (BME) reports record Christmas trading with like-for-like sales in its core UK B&M estate up 3.9%.

While this does represent a slowing of growth from the first half rate, the strong performance builds on last year’s strong third quarter comparator, when UK like-for-likes shot up 7.2%.

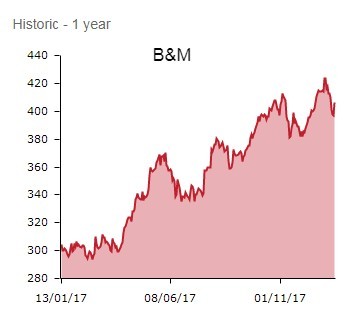

In a week when several rival retail updates were poorly received, investors are suitably impressed and the news sends high-flying shares in the Liverpool-headquartered discounter up 2.4% (9.6p) to 406.5p.

An update for the third quarter to 23 December reveals 12.9% growth to £837.3m in the B&M store estate, reflecting same-store growth and new store openings.

IN THE VANGUARD OF VALUE

As the variety retailer, floated on the stock market in 2014 with retail grandee Sir Terry Leahy as chairman, explains: ‘The strong like-for-like performance in the quarter reflects the continued robust performance of our grocery and FMCG (fast moving consumer goods) ranges, further operational improvements to store standards for customers and the recognition of our value offer by consumers generally.'

The FTSE 250 constituent also says the recently acquired UK convenience chain Heron chipped in £79.8m of revenues in the quarter, including ‘strong positive like-for-like revenue growth’.

Over in Germany, B&M's Jawoll chain’s sales grew 10.4% to £52.7m in sterling terms, Christmas ranges sourced from the far east flying off the shelves.

CEO Simon Arora is confident his charge will meet EBITDA market expectations for the year to March, with consensus pitched at £284m for 21% year-on-year growth.

Arora insists ‘B&M continues to go from strength to strength. Despite the demanding comparatives from the very strong Christmas in 2016, our buying, supply chain and retail teams achieved another outstanding performance this year by doing what we do best, which is delivering great value for customers week-in, week-out.’

THE ANALYSTS’ VIEW

‘Retail’s big week comes to a close on a high with B&M reporting a blockbuster third quarter following the departure of Sir Terry Leahy,’ comments Neil Wilson, Senior Market Analyst at ETX Capital.

‘The discounter managed to deliver a healthy boost to UK sales as efforts to build its out presence in southern England start to pay off. Crucially, B&M continued to growth UK like-for-like sales at a healthy clip and this marks it out as one the top store-based performers over the last 12 months, although we did not get a repeat of the exceptional quarter-on-quarter LFL sales growth reported in Q2.'

Wilson adds B&M's 'ambitious store expansion programme is paying off and shows there is still room on the high street for brands that can meet consumers’ needs effectively.'

'We expect organic growth combined with the ongoing store roll-out to support long-term double-digit growth across the UK and in Germany. B&M offers exposure to a self-funded, integrated, high growth and cash generative business, which is one of the highest quality names in UK retail.'