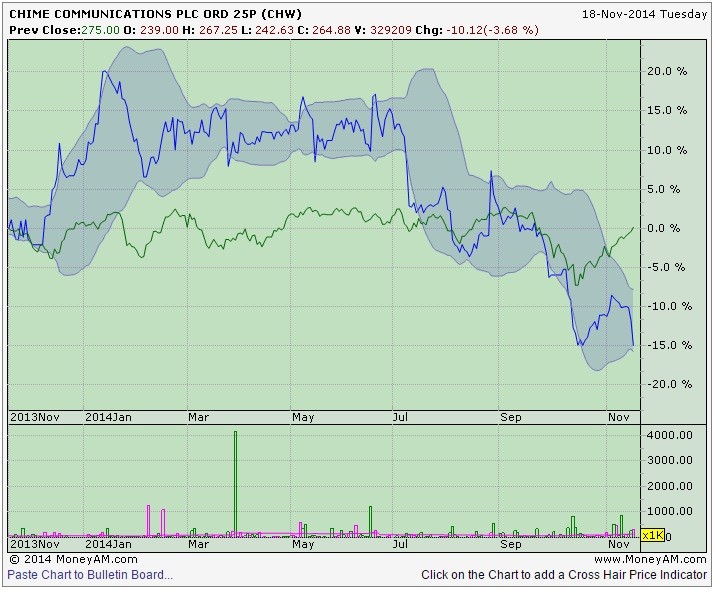

Communications and sports marketing play Chime Communications (CHW) is down 4.6% to 262.25p as it warns on 2014 profits. The relatively modest sell-off - earlier the stock was down as much as 11% - probably reflects the fact that 2015 guidance remains intact and the analyst community is still broadly on side.

In its interim management statement covering the period from 1 July to 17 November the company reveals two significant contracts in its Sports & Entertainment division are now set to commence in 2015 rather than 2014. So although operating profit is still expected to grow by 20% year-on-year, this is around 20% short of what had been pencilled in.

The £261 million cap's exposure to major events like the football World Cup and Olympics means it has a stepped earnings profile with limited growth in ‘odd’ years and stellar performance in ‘even years’ to reflect when these tournaments typically fall. In this context CanaccordGenuity says that despite the fact profits are still set to increase 'this remains a disappointing outcome for a World Cup year'. The broker cuts its price target from 385p to 370p but retains its buy recommendation.

Investec also stays at buy but puts its target under review noting: 'The outlook for FY15 is unchanged assuming these contracts are signed then. Chime is contracting for increasingly large global contracts, which move the dial more aggressively, but can take time to sign/deliver. Early contract wins for the Rio Olympic Games suggest a strong FY16E outlook.'

Numis reiterates its buy take and 413p price target and says: 'Chime reiterates its guidance for 2015 and we retain our estimates of £38.5 million/27.2p (PBT/EPS), which we expect to prove conservative as the delayed 2014 contracts come through. Given strong underlying progress during the year, the delay to the major 2014 contracts is disappointing though we remain supportive of the group's expansion into Sports & Entertainment while the other divisions are performing to plan.'