A tricky week for US stocks ended on a brighter note as some dovish messaging from US Federal Reserve chair Jerome Powell helped lift technology stocks.

While Powell suggested the Fed was not done yet with rate hikes in testimony before US lawmakers he did at least suggest he and his colleagues would proceed with caution.

Financial markets are largely pricing in a 25 basis point hike at the conclusion of the Fed's next meeting on 26 July. Until then, when we should also start getting the first round of second quarter earnings from the US, markets could struggle for direction.

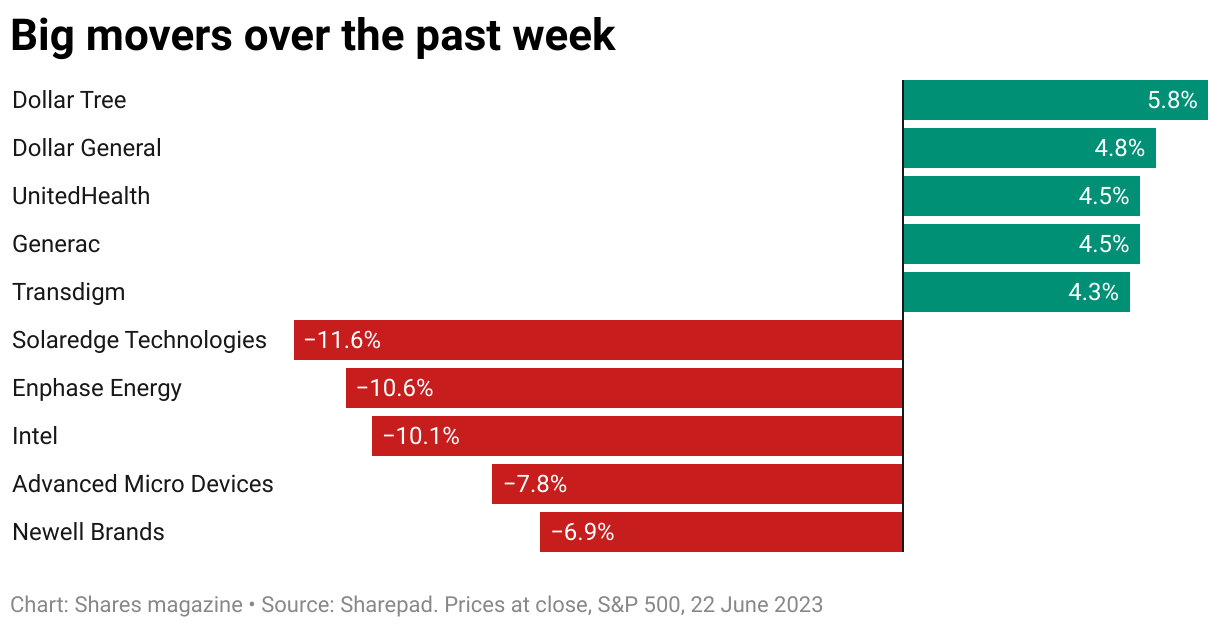

At a company level, bargain hunters were out in force for some stocks which have been the focus of heavy selling of late. This included UnitedHealth (UNH:NYSE), recently pegged as being hit by an increase in costs associated with a pick up in elective surgeries among elderly Americans coming out of the pandemic.

Discount stores Dollar General (DG:NYSE) and Dollar Tree (DLTR:NASDAQ), both clobbered on weak quarterly updates in the last few weeks, also bounced back a touch.

The reverse was true for chipmakers Intel (INTC:NASDAQ) and Advanced Micro Devices (AMD:NASDAQ) as some of the excitement around the industry and the potential boost from an AI (artificial intelligence) arms race faded.

FEDEX

Delivery giant FedEx (FDX:NYSE) gave investors a scare this week despite delivering fourth quarter earnings ahead of Wall Street expectations.

The company gave a very cautious outlook for the year to 31 May 2024 as it guided for flat to low single digit revenue growth and EPS (earnings per share) to be at the lower end of the $16.50 to $18.50 range.

The forecast fell short of analyst expectations which are pegged at $18.4 according to Refinitiv data, implying future downward earnings revisions.

Fedex is an integral cog in the workings of world trade and provides a unique window into the general health of the world economy, so its downbeat outlook shouldn’t be taken lightly.

The company reported a 28% drop in fourth quarter EPS to $4.94 which marginally beat Wall Street estimates of $4.89 while revenue fell 10% to $21.93 billion, slightly less than estimates of $22.67 billion.

After falling 3% in after hours trading the shares regained some form and remain up 32% for the year.

ROYAL CARIBBEAN CRUISES

The travel industry struggled between 2020 to 2022 from a stop-start recovery yet 2023 looks to go down in the history as the year when the sector finally got back on track after Covid-19. Shares in Royal Caribbean Cruises (RCL:NYSE) this week hit their highest level since February 2020 as investors scour the travel sector for ways to play the rebound in demand. In May, the cruise operator increased its full-year guidance after saying that bookings were being made at higher prices and customers were spending more than expected once onboard.

Chief executive Jason T. Liberty said demand was ‘well above historical trends and at higher rates.’ Its second-quarter results will be published on 2 July where analysts currently expect $3.4 billion revenue and $431 million pre-tax profit (Q2 2022: $530 million loss) .While everything appears to be going swimmingly for the cruise industry, there is a risk that customers finish the summer with a sour taste.

Widespread reports of ships full to capacity means crowding and discomfort among passengers. Investors don’t appear to be worried about these issues as they’re simply focused on the profits which are expected to keep rising near-term.

TESLA

Investors have just become too optimistic too quickly on Tesla (TSLA:NASDAQ) for Barclays. A run of electric vehicle (EV) charging deals with Ford (F:NYSE), General Motors (GM:NYSE) and Rivian Automotive (RIVN:NASDAQ) have helped to supercharge the stock, which has rallied nearly 7% over the past week.

Morgan Stanley recently estimated that the charging network could be worth more than $100 billion by 2030.But Barclays analyst Dan Levy thinks there are near-term challenges that could drag on the stock.

More price cuts are possible as Tesla tries to seed EV sales in a sagging economy and fend off rising competition, but this would pressure profit margins and earnings that are already creaking.

In April, Tesla reported first quarter gross profit margins of 19.3%, compared with expectations of 22.4% expected, the lowest since the fourth quarter of 2020.Levy sees Tesla EPS (earnings per share) of $4 in 2024. The Wall Street consensus is at $5.03, based on Koyfin data.

Even if Tesla does earn close to the average, the recent rally (up 42% in a month) to $265 has taken the stock’s PE (price to earnings) multiple to about 53 times estimated 2024 numbers, from 38 a month ago.‘The relative disregard of challenges to near-term Tesla fundamentals amid the sharp rally is our key concern for the stock,’ wrote Levy.